The engineering manager works closely with the production manager to ensure that new technologies and processes are integrated into the production process and that efficiency variance is minimized. The engineering manager is responsible for developing and implementing new technologies and processes to improve production efficiency. In that case, it may be a sign that something is not working as it should be. In this case, the company should investigate the cause of the variance and take action to address it. This could involve identifying bottlenecks in the production process, re-evaluating staffing levels, or implementing new technologies or processes to improve efficiency.

© Accounting Professor 2023. All rights reserved

Cross-training can also help to improve communication and collaboration among employees. If the cost of maintaining and repairing current equipment is high, investing in new equipment may be more cost-effective in the long run. New equipment may require less maintenance and repairs, reducing costs and improving efficiency.

Increased Costs – Risks Associated With Ignoring Efficiency Variance

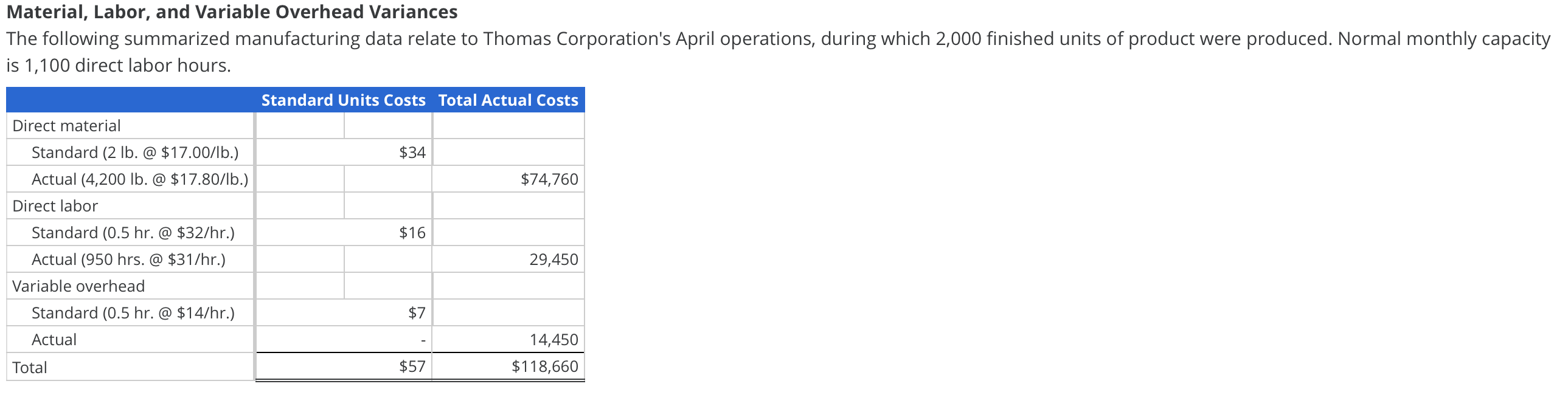

The standard variable manufacturing overhead rate is $3 per direct labor hour. Each unit should require 0.25 direct labor hours for total variable manufacturing overhead costs per unit of $0.75. It is important to note that cost standards are established before the work is started. Production managers are responsible for controlling costs and meeting the target cost, which is $7.35 per unit in this case. The total direct materials cost variance is also found by combining the direct materials price variance and the direct materials quantity variance.

Poor Communication – Potential Roadblocks A Company May Encounter When Addressing Efficiency Variance

A negative material yield variance, on the other hand, means that the company has used more material than expected, indicating that there may be opportunities to reduce waste and improve efficiency. Hence, variance arises due to the difference between actual time worked and the total hours that should have been worked. Let’s also assume that the quality of the low-cost denim ends up being slightly lower than the quality to which your company is accustomed. This lesser quality denim causes the production to be a bit slower as workers spend additional time working around flaws in the material.

Efficiency variance can lead to non-compliance with industry regulations and standards. Ignoring efficiency variance can result in continued non-compliance, leading to fines, legal issues, and damage to the company’s reputation. When investing in new equipment, evaluating the potential return on investment (ROI) is essential.

Causes of unfavorable direct materials quantity variance

- A manufacturer must disclose in its financial statements the cost of its work-in-process as well as the cost of finished goods and materials on hand.

- Direct material and direct labor are considered variable manufacturing costs, since the total amount for these costs changes based on production.

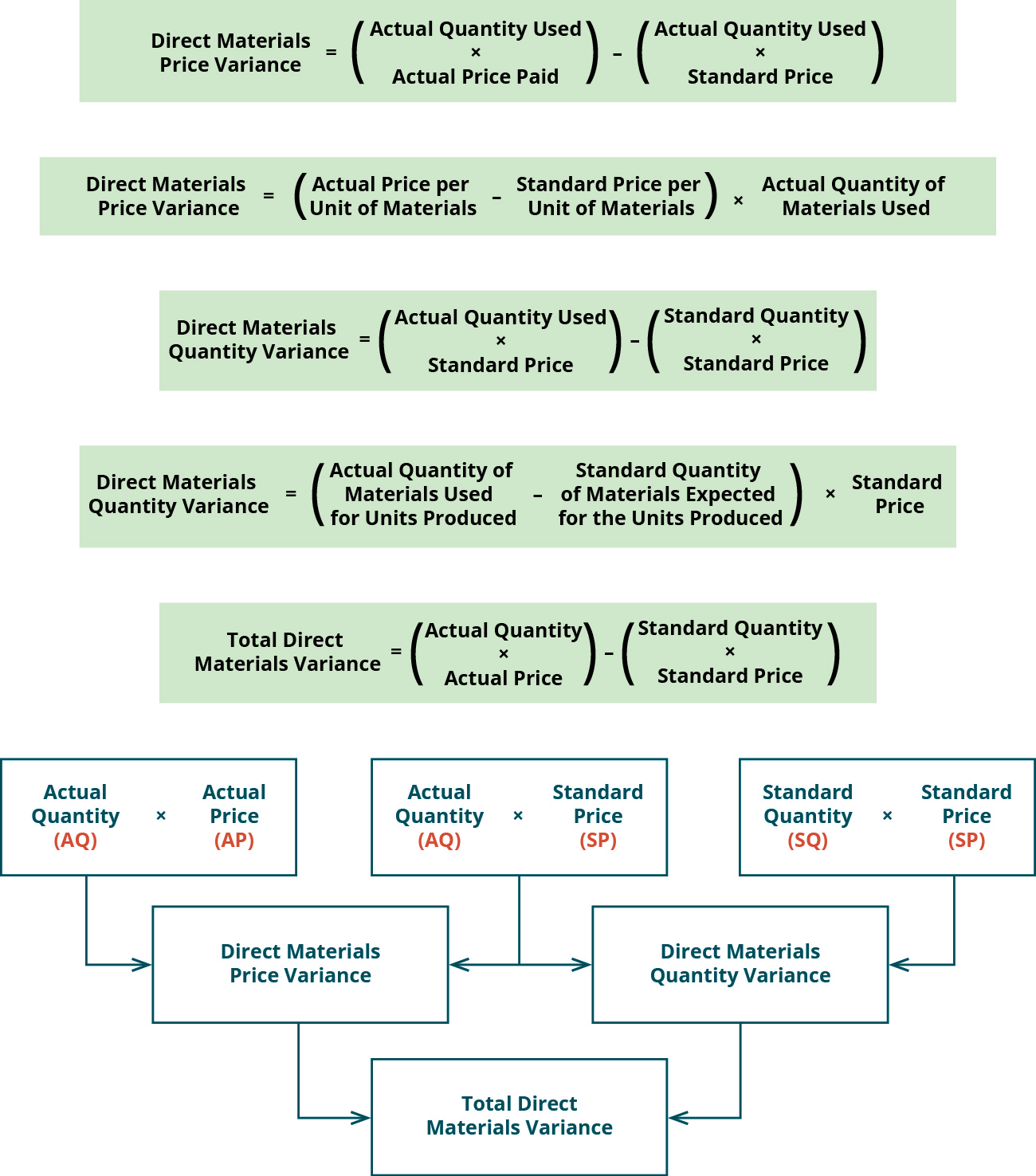

- The total direct materials variance is calculated as the total standard costs allowed for direct materials of $315,000 less the actual amount paid of $330,000 equal the total direct materials variance of $(15,000) U.

- In order to calculate the direct materials usage (or quantity) variance, we start with the number of acceptable units of products that have been manufactured—also known as the good output.

- If $2,000 is an insignificant amount relative to a company’s net income, the entire $2,000 unfavorable variance can be added to the cost of goods sold.

The total price per unit variance is the standard price per unit of $0.50 less the actual price paid of $0.55 equals the price variance per unit of $(0.05) U. This is unfavorable because they actually spent more per unit than the standards allowed. The example of the NoTuggins dog harness is used throughout this chapter to illustrate standard costs and standard costs variances for product costs. Brad invented NoTuggins, a revolutionary dog harness that stops dogs from pulling when connected to a leash by humanely redistributing the dog’s pulling force. NoTuggins was featured as the most innovative new harness by the International Kennel Association.

This shows that we saved money by buying cheaper, but lost money because of material waste. It could be that the cheaper lumber has more knots, therefore forcing workers to throw more of the raw materials in the scrap heap. The responsible managers (e.g. purchasing and production) will have to get together to do more observations and research. It may also be that our expectations are unrealistic and we need to change our budget parameters.

As mentioned previously, standard rates and quantities are established for variable manufacturing overhead. When discussing variable manufacturing overhead, price is referred to as rate, and quantity is referred to as efficiency. These standards are compared to the actual quantities used and the actual rate paid for variable manufacturing overhead using the same processes applied in previous sections to analyze direct materials and annuity present value formula calculator direct labor. Any variance between the standard costs allowed and the actual costs incurred is caused by a difference in efficiency or a difference in rate. The total variance for variable manufacturing overhead is separated into the variable manufacturing overhead efficiency variance and the variable manufacturing overhead rate variance. The variable manufacturing overhead variances for NoTuggins are presented in Exhibit 8-10.

This would be a theoretical standard, that can only be met if the circumstances are optimal. Or, a realistic standard could be used that incorporates reasonable inefficiency levels, and which comes close to actual results. Generally, the latter approach is preferable, if only to avoid a depressing series of negative efficiency variances. Due to the higher than planned hourly rate, the organization paid $22,500 more for direct labor than they planned. This variance should be investigated to determine if the actual wages paid for direct labor can be lowered in future periods or if the standard direct labor rate per hour needs to be adjusted. For example, an investigation could reveal that the company had to pay a higher rate to attract employees, so the standard hourly direct labor rate needs to be adjusted.

By calculating efficiency variance for different areas of the production process, companies can identify areas where improvements can be made to increase efficiency and productivity. This can involve implementing best practices, such as lean manufacturing, continuous improvement, and data analytics, to identify and address inefficiencies in their processes. Efficiency variance is essential in the manufacturing industry because it can impact a company’s profitability and competitiveness. High levels of efficiency variance can result in increased costs, lower productivity, and reduced quality, leading to lost revenue and decreased customer satisfaction. Accountants determine whether a variance is favorable or unfavorable by reliance on reason or logic. This could be for many reasons, and the production supervisor would need to determine where the variable cost difference is occurring to better understand the variable overhead reduction.

The Direct Materials Inventory account is reduced by the standard cost of the denim that was removed from the direct materials inventory. Let’s assume that the actual quantity of denim removed from the direct materials inventory and used to make the aprons in January was 290 yards. Because Direct Materials Inventory reports the standard cost of the actual materials on hand, we reduce the account balance by $870 (the 290 yards actually used x the standard cost of $3 per yard). After removing 290 yards of materials, the balance in the Direct Materials Inventory account as of January 31 is $2,130 (710 yards x the standard cost of $3 per yard).